{kind=link}

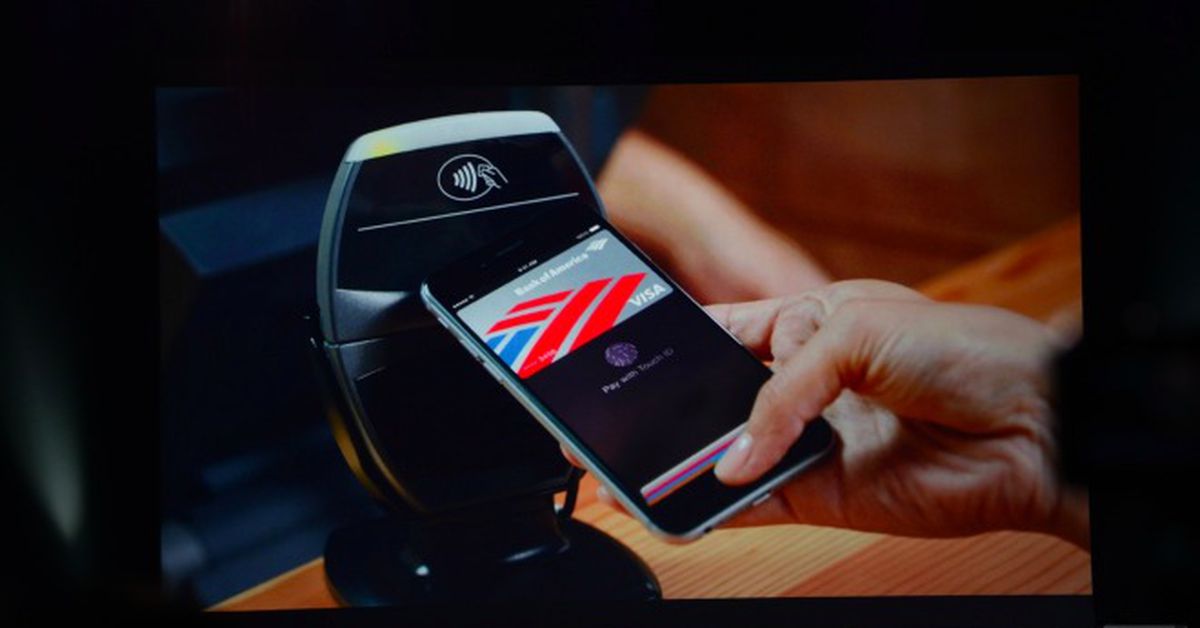

When Apple launched Apple Pay in 2014, at an occasion 10 years to the day earlier than this yr’s iPhone launch, Apple promised the function would “change the way in which you pay.” The corporate didn’t simply allow you to save a bank card quantity in your telephone; it allow you to pay for issues with a single faucet by transmitting data by an NFC chip. Apple was so bullish on cellular funds that Apple Pay was even one of many key promoting factors for the also-just-announced Apple Watch.

A decade later, Apple Pay is in all places. You should utilize it to purchase groceries and occasional; you should utilize it to experience the New York Metropolis subway or lease a Lime scooter. You should utilize Apple Pay and skip the entire multipage checkout course of on a lot of on-line shops. You should utilize it in your telephone, your watch, your laptop, numerous web sites, your TV, and your headset. The Client Monetary Safety Bureau estimated that 55.8 million People made an in-store fee with Apple Pay within the month of April 2023. Apple says Pay works at greater than 85 % of shops within the US, however anecdotally, I can’t keep in mind the final time I couldn’t pay simply by double-clicking the ability button on my telephone. Apple Pay is so good, it may be harmful.

Apple Pay is without doubt one of the most Apple-y Apple merchandise the corporate has ever shipped. It was, and is, a examine in each the ability of integration and Apple’s distinctive means to get its approach in a aggressive business. Whereas Google flailed round with its personal cellular funds system — which has been Google Pockets and Google Pay and Android Pay and I feel Google Pockets once more, and truthfully who can preserve monitor anymore? — Apple simply relentlessly iterated on Apple Pay till it turned each nice and ubiquitous. It’s gotten slightly bloated as Apple has regarded for extra methods to make it worthwhile: Apple Pay begot Apple Money and the Apple Card and Apple Pay Later and Apple’s complete concept about digital ID playing cards, which have all labored someplace between “form of fantastic” and “in no way.”

And possibly most Apple-y of all, Apple Pay has been ruthlessly managed and locked down by its creator. Different builders haven’t been in a position to entry the tap-to-pay options, so you possibly can’t pay immediately from any app apart from Apple Pockets. Builders haven’t any different alternative however so as to add playing cards to Apple Pockets (and thus pay the 0.15 % payment for every credit score transaction). You possibly can’t change the app that seems if you double-tap the ability button, both, not that you’d, as a result of no one can construct a aggressive cellular pockets app with out tap-to-pay. Have you ever ever observed that there aren’t any Apple Pockets rivals? They merely aren’t allowed to exist.

Apple has argued, because it at all times does, that these restrictions existed within the identify of safety and privateness, however critics say they’re truly about processing charges and platform lock-in. Apple Pay was even named as a core tenet of the US authorities’s antitrust case towards Apple. “Whereas Apple actively encourages banks, retailers, and different events to take part in Apple Pockets, Apple concurrently exerts its smartphone monopoly to dam these identical companions from growing higher fee services for iPhone customers,” the Division of Justice wrote in its preliminary antitrust grievance earlier this yr.

Apple Pay is about to turn out to be the proper check case for the way forward for Apple

A decade after its launch, Apple Pay is about to turn out to be the proper check case for the way forward for Apple. After the antitrust case within the US and a collection of recent guidelines within the EU, Apple introduced that starting with iOS 18.1, third-party builders will be capable to allow tap-to-pay transactions in their very own apps. Customers may also be capable to set a default app for contactless funds and alter what occurs after they double-click the ability button. There will likely be hoops for builders to leap by and costs for them to pay, however the chip will likely be obtainable.

Opening up NFC entry has the potential to show tap-to-pay into tap-to-everything. For years, Apple and others have talked about wanting to show all of your keys, ID playing cards, loyalty playing cards, tickets, reward playing cards, and extra into digital objects you can transmit or share with a faucet. Till now, that hasn’t actually taken off, however many builders would possibly now be fascinated with constructing these instruments as a result of they’ll construct them into their very own app. Banks and fintech corporations would possibly add tap-to-pay so you possibly can pay from the identical place you handle your cash. Perhaps you’ll be capable to get right into a bar, on a flight, into your automobile, or into your workplace with just a few faucets. Perhaps each file sharing system will assist NFC, so you possibly can faucet your good friend a photograph or PDF. Perhaps the NFC chip will turn out to be as core part of the iPhone’s worth because the GPS chip or the digicam, the continuing connection between your system and the actual world. And possibly, as a result of Apple has such cultural energy inside the tech business, will probably be the catalyst for digitizing these different programs in all places.

Opening up NFC entry has the potential to show tap-to-pay into tap-to-everything

Or possibly opening up the system would possibly damage the entire thing. Perhaps, as an alternative of a single place with all of your playing cards that seems anytime you press a button, you must obtain, log in to, and handle each single fee choice in your life in a completely totally different app. Perhaps some corporations will assist third-party wallets and a few gained’t, so that you’ll must do not forget that your Visa and AMC Stubs card are right here however your Uncover card and library card are over there. Perhaps there will likely be big safety flaws in how all of those corporations handle issues, and corporations will start to gather huge quantities of information you’d quite not give them. Perhaps they’ll cease supporting Apple Pockets — as a result of processing charges! — and power you into their ugly, gradual, ad-filled, upselling apps. Perhaps Apple wasn’t simply moneygrubbing and was, actually, stopping the true moneygrubbers from making cellular funds unusable.

These are believable outcomes, and there are some much less excessive potentialities, too. However we’re about to see Apple confront this new world in so some ways: as the corporate is pressured to alter its App Retailer guidelines, give builders entry to beforehand unavailable system options, and permit customers to choose extra of their very own defaults, the query is identical throughout each floor. Was Apple’s legendarily tight management about preserving person expertise and ensuring customers obtained the perfect of every thing with the least quantity of labor, or was it about Apple making its gadgets worse simply to make them tougher to stop? Nobody’s ever had a good combat with Apple earlier than. However the taking part in discipline is starting to stage.